Mục lục . Content

- 1. Decree 218/2013/ND-CP on Enterprises Income Tax

- Chapter I. GENERAL PROVISIONS

- Chapter II . TAX BASES AND TAX CALCULATION METHODS

- Article 5. Tax bases

- Article 6. Determination of taxed incomes

- Article 7. Determination and carrying forward of losses

- Article 8. Turnover

- Article 9. Deductible and non-deductible expenses upon determination of taxable incomes

- Article 10. Tax rates

- Article 11. Tax calculation method

- Article 12. Places for tax payment

- Chapter III. INCOMES FROM REAL ESTATE TRANSFER

- Article 13. Incomes from real estate transfer include income from the transfer of land use or lease rights; income from sublease of land of real estate-trading enterprises in accordance with the land law, regardless of whether infrastructure or architectural works attached to land are available or not; income from the transfer of houses or construction works attached to land, including assets attached to such houses or construction works, regardless of whether land use or lease rights are transferred or not; and income from the transfer of other assets attached to land.

- Article 14. Taxable income from real estate transfer is turnover from real estate transfer activities minus the cost price of real estate and deductible expenses related to the real estate transfer.

- Chapter IV. ENTERPRISE INCOME TAX INCENTIVES

- Chapter V. IMPLEMENTATION PROVISIONS

- Appendix. LIST OF LOCALITIES ELIGIBLE FOR ENTERPRISE INCOME TAX INCENTIVES

- 2. Decree 91/2014/ND-CP (Amending Decree 218/2013/ND-CP)

- Article 1. To amend, supplement the Decree No. 218/2013/ND-CP dated December 26, 2013 of the Government detailing the implementation of the law on enterprise income law as follows:

- 1. To amend, supplement Point m Clause 2 Article 3 as follows:

- 2. To amend, supplement Clause 3 Article 4 as follows:

- 3. To amend, supplement Clause 9 Article 4 as follows:

- 4. To amend, supplement Point a Clause 1 Article 9 as follows:

- 5. To amend, supplement Point d Clause 2 Article 9 as follows:

- 6. To amend, supplement Clause 3 Article 16 as follows:

- 7. To supplement Clause 5a Article 19 as follows:

- 8. To supplement Clause 5b Article 19 as follows:

- 9. To amend Point 2, 3, 4, 5, 32, 37 of the list of areas entitled to preferential of enterprise income tax under the Appendix promulgated together with the Decree No. 218/2013/ND-CP as follows:

- Article 5. Effect

- 3. Decree 12/2015/ND-CP (Amending Decree 218/2013/ND-CP)

- Article 1. To amend and supplement a number of articles of Decree No. 218/2013/ND-CP …

- 1. To amend and supplement Clause 3, Article 3 as follows:

- 2. To amend and supplement Clause 1, Article 4 as follows:

- 3. To supplement Clause 9, Article 4 as follows:

- 4. To add Clause 12 to Article 4 as follows:

- 5. To supplement Point a, Clause 1, Article 9 as follows:

- 6. To amend and supplement Point e, Clause 2, Article 9 as follows:

- 7. To amend Point o, Clause 2, Article 9 as follows:

- 8. To amend and supplement Clause 1, Article 11 as follows:

- 9. To amend and supplement Point dd, Clause 1, Article 15 as follows:

- 10. To supplement Point e, Clause 1, Article 15 as follows:

- 11. To add Point g to Clause 1, Article 15 as follows:

- 12. To amend and supplement Point a, Clause 2, Article 15 as follows:

- 13. To amend and supplement Point dd, Clause 2, Article 15 as follows:

- 14. To supplement Clause 3a, Article 15 as follows:

- 15. To supplement Clause 5a, Article 15 as follows:

- 16. To amend and supplement Point a, Clause 1, Article 16 as follows:

- 17. To supplement Point dd, Clause 2, Article 19 as follows:

- 18. To amend and supplement Clause 5, Article 19 as follows:

- 19. To add Clause 6 to Article 19 as follows:

- 20. To amend and supplement Clause 2, Article 20 as follows:

- Article 6. Effect and implementation responsibility

- 4. Decree 146/2017/ND-CP (Amending Decree 218/2013/ND-CP)

- 5. Decree 57/2021/ND-CP (Amending Decree 218/2013/ND-CP)

1. Decree 218/2013/ND-CP on Enterprises Income Tax,

2. Decree 91/2014/ND-CP (Amending Decree 218/2013/ND-CP),

3. Decree 12/2015/ND-CP (Amending Decree 218/2013/ND-CP),

4. Decree 146/2017/ND-CP (Amending Decree 218/2013/ND-CP),

5. Decree 57/2021/ND-CP (Amending Decree 218/2013/ND-CP).

—

(English – Tiếng Anh)

1. Decree 218/2013/ND-CP on Enterprises Income Tax

DECREE 218/2013/ND-CP

December 26, 2013

Detailing and guiding the implementation of

the Law on Enterprise Income Tax

Pursuant to the December 25, 2001 Law on Organization of the Government;

Pursuant to the June 3, 2008 Law on Enterprise Income Tax and the June 19, 2013 Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax;

At the proposal of the Minister of Finance,

The Government promulgates the Decree to detail and guide the implementation of the Law on Enterprise Income Tax.

Chapter I. GENERAL PROVISIONS

Article 1. Scope of regulation

This Decree details and guides the implementation of a number of articles of the Law on Enterprise Income Tax and the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax on taxpayers; taxable incomes, tax-exempt incomes; determination of taxed incomes, determination and carrying forward of losses; turnover; deductible and non-deductible expenses upon determination of taxable incomes; tax rates; tax calculation method; tax incentives and conditions for application of tax incentives.

Article 2. Taxpayers

Taxpayers are defined in Article 2 of the Law on Enterprise Income Tax and Clause 1, Article 1 of the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax.

1. Taxpayers defined in Clause 1, Article 2 of the Law on Enterprise Income Tax include:

a/ Enterprises established and operating under the Law on Enterprises, the Law on Investment, the Law on Credit Institutions, the Law on Insurance Business, the Law on Securities, the Law on Petroleum, the Commercial Law, and other legal documents, in the form of joint-stock company; limited liability company; partnership; private enterprise; party to business cooperation contract; party to oil and gas production sharing contract, oil and gas joint-venture enterprise or jointly operating company;

b/ Enterprises established under foreign laws (below referred to as foreign enterprises) with or without Vietnam-based permanent establishments;

c/ Public or non-public non-business units producing and trading in goods or providing services and having taxable incomes under Article 3 of this Decree;

d/ Organizations established and operating under the Law on Cooperatives;

dd/ Organizations other than those defined at Points a, b, c and d of this Clause that carry out production and business activities and have taxable incomes under Article 3 of this Decree.

2. Organizations established and operating (or registering operation) under Vietnamese law, business individuals paying tax by the withholding method in case of purchase of services (including services associated with goods, purchase of goods supplied or distributed in the form of on-the-spot import and export or according to international commercial terms) on the basis of contracts signed with foreign enterprises defined at Points c and d, Clause 2, Article 2 of the Law on Enterprise Income Tax.

The Ministry of Finance shall specifically guide the tax withholding referred to in this Clause.

Article 3. Taxable incomes

1. Taxable incomes include income from goods production and trading and service provision and other incomes specified in Clause 2 of this Article. For enterprises having registered their business and earning incomes specified in Clause 2 of this Article, such incomes will be determined as incomes from their production and business activities.

2. Other incomes include:

a/ Income from capital transfer, including income from the transfer of part or the whole of the capital amount invested in an enterprise, even in case of sale of enterprises, transfer of securities, transfer of the capital contribution right and transfer of capital in other forms in accordance with law;

b/ Income from transfer of investment projects, income from transfer of the right to join investment projects, income from transfer of the mineral exploration, exploitation or processing right in accordance with law; income from transfer of real estate under Articles 13 and 14 of this Decree;

c/ Income from the right to use or own assets, including income from intellectual property rights and income from technology transfer in accordance with law;

d/ Income from transfer, lease or liquidation of assets (except real estate), including other valuable papers;

dd/ Income from deposit interests, loan interests or foreign currency sales, including interests on deposits at credit institutions, interests on loans in any forms in accordance with law, including interests on deferred or installment payments, credit guarantee charges and other charges in loan provision contracts; income from foreign currency sales; exchange rate differences resulting from the revaluation of payable debts of foreign-currency origin at the end of a fiscal year; foreign exchange rate differences arising in a period (particularly, foreign exchange differences arising in the process of capital construction investment to form fixed assets of newly established enterprises which are not yet put into production or business activities shall comply with the guidance of the Ministry of Finance). Foreign exchange rate differences of receivable debts or loans of foreign-currency origin arising in a period are differences between foreign exchange rates at the time of debt collection and those at the time of recording receivable debts or initial loans;

e/ Amounts deducted in advance as expenses which are left unused or have not been used up in the period of their deduction and not accounted by enterprises to reduce expenses;

g/ Recovered bad debts which have been written off;

h/ Payable debts of unidentifiable creditors;

i/ Omitted incomes from previous years’ business activities now discovered;

k/ Difference between collected fines or compensations for breaches of economic contracts or rewards for proper realization of contract commitments (excluding fines and compensations recorded as reductions of the work value in the stage of investment) and paid fines or compensations for contract breaches in accordance with law;

l/ Received aid in cash or in kind;

m/ Differences resulting from the revaluation of assets in accordance law for capital contribution or transfer upon separation, split, merger, consolidation or transformation of enterprises.

Asset-receiving enterprises may conduct accounting based on revaluation prices when determining deductible expenses specified in Article 9 of this Decree;

n/ Incomes from production and business activities carried out outside Vietnam;

o/ Other incomes, including tax-exempt incomes, specified in Clauses 6 and 7, Article 4 of this Decree.

3. Taxable incomes generated in Vietnam by foreign enterprises defined at Points c and d, Clause 2, Article 2 of the Law on Enterprise Income Tax are incomes originating in Vietnam received from the provision of services, supply and distribution of goods, provision of loans and copyright royalties collected from Vietnamese organizations and individuals or foreign organizations and individuals doing business in Vietnam, regardless of their places of business.

Taxable incomes specified in this Clause exclude income from services provided outside the Vietnamese territory, such as overseas repair of means of transport, machinery or equipment; overseas advertising, marketing and investment and trade promotion; overseas goods or service sale brokerage; overseas training; and international post and telecommunications service charges divided to foreign parties.

The Ministry of Finance shall specifically guide taxable incomes referred to in this Clause.

Article 4. Tax-exempt incomes

Tax-exempt incomes are specified in Article 4 of the Law on Enterprise Income Tax and Clause 3, Article 1 of the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax.

1. Incomes from cultivation, husbandry, aquaculture or salt production of cooperatives; incomes of cooperatives operating in the sector of agriculture, forestry, fisheries or salt production in localities with difficult socio-economic conditions or localities with particularly difficult socio-economic conditions; incomes of enterprises from cultivation, husbandry or aquaculture in localities with particularly difficult socio-economic conditions; incomes from marine fishing.

Tax-exempt incomes from cultivation, husbandry or aquaculture of cooperatives and enterprises specified in this Clause exclude incomes from the processing or production of products from cultivation, husbandry or aquaculture. Cooperatives and enterprises shall separately account incomes from cultivation, husbandry or aquaculture from other processing or production stages in order to determine enterprise income tax-exempt amounts mentioned in this Clause. In case it is impossible to separately account such incomes, tax-exempt incomes may be determined according to the ratio of expenses for tax-exempt activities to the total production and business expenses in a tax period.

Tax-exempt cultivation, husbandry or aquaculture activities of cooperatives and enterprises in localities with particularly difficult socio-economic conditions specified in this Clause and at Point e, Clause 2, Article 15 of this Decree shall be determined based on the level-1 economic sector codes of agriculture, forestry and aquaculture prescribed in the System of Economic Sectors of Vietnam.

Cooperatives operating in the sector of agriculture, forestry, fisheries or salt production specified in this Clause and Clause 2, Article 15 of this Decree are those satisfying the condition of ratio of products or services provided to their members being individuals, households or legal persons engaged in agriculture, forestry, fisheries or aquaculture in accordance with the Law on Cooperatives and guiding documents.

2. Tax-exempt incomes from the provision of technical services directly for agriculture include income from services of irrigation and water drainage, soil plowing and harrowing, dredging of in-field canals and ditches, prevention and control of crop and animal pests and diseases, and harvest of agricultural products.

3. For incomes from the performance of scientific research and technology development contracts, sale of products turned out from trial production and with technologies applied for the first time in Vietnam, the maximum tax exemption duration is one year from the date of generating turnover from the sale of products under scientific research and technology application contracts, trial production or production with new technologies.

The Ministry of Finance shall specifically guide this Clause.

4. Incomes from goods production and trading and service provision activities of enterprises employing disabled, detoxified and HIV/AIDS-affected persons who account for at least 30% of the average number of employees in a year.

Tax-exempt enterprises specified in this Clause are those having an average number of employees of at least 20 in a year, excluding those operating in the fields of finance and real estate business.

Tax-exempt incomes specified in this Clause exclude other incomes specified in Clause 2, Article 19 of this Decree.

5. Incomes from vocational training activities exclusively reserved for ethnic minority people, the disabled, children in extremely disadvantaged circumstances, persons involved in social evils, persons undergoing detoxification, detoxified persons and HIV/AIDS-affected persons. If an establishment also provides vocational training for other categories of people, tax-exempt income will be determined based on the ratio between the number of ethnic minority people, the disabled, children in extremely disadvantaged circumstances, persons involved in social evils, persons undergoing detoxification, detoxified persons and HIV/AIDS-affected persons and the total number of job trainees of the establishment.

6. Incomes divided from capital contribution, share purchase, joint venture or association with domestic enterprises, after contributed capital recipients, bond issuers or joint-venture or association parties, including those enjoying tax incentives under Chapter IV of this Decree, have paid tax in accordance with the Law on Enterprise Income Tax.

7. Received aid for use for educational, scientific research, cultural, artistic, charitable, humanitarian and other social activities in Vietnam.

Aid beneficiaries that improperly use the aid shall pay enterprise income tax calculated on the improperly used aid amount in the tax period during which the aid is improperly used.

Aid beneficiaries defined in this Clause are organizations established and operating in accordance with law and strictly observing the laws on accounting and statistics.

8. Incomes from the first-time transfer of Carbon Emission Reduction Certificates (CERs) of enterprises which have been granted such certificates. For subsequent transfers, enterprises shall pay enterprise income tax.

9. Incomes from the performance of state-assigned tasks of the Development Bank of Vietnam regarding development investment credit and export credit; incomes from the Social Policy Bank’s activities of providing credit to the poor and other policy beneficiaries; incomes of the single-member limited liability company managing assets of Vietnamese credit institutions (VAMC); incomes from revenue-earning activities in the performance of state-assigned tasks of the state financial funds: the Vietnam Social Security Fund, the Deposit Insurance, the Health Insurance Fund, the Vocational Training Support Fund, the Overseas Employment Support Fund under the Ministry of Labor, War Invalids and Social Affairs, the Supporting Fund for Farmers, the Vietnam Legal Aid Fund, the Vietnam Public-Utility Telecommunications Service Fund, local development investment funds, the Vietnam Environmental Protection Fund, the Credit Guarantee Fund for Small- and Medium-Sized Enterprises, the Cooperative Development Support Fund, the Assistance Fund for Poor Women, the Fund for Assisting Overseas Vietnamese Citizens and Legal Entities, the Housing Development Fund, the Fund for Development of Small- and Medium-Sized Enterprises, the National Foundation for Science and Technology Development, and the National Technology Innovation Fund; incomes from the performance of state-assigned tasks of the Land Development Fund and other not-for-profit funds of the State which are established under decisions of the Government or the Prime Minister and operate in accordance with law.

10. Undivided incomes of establishments engaged in socialized education and training, health and other socialized fields (including judicial assessment offices) which are retained for investment in such establishments in accordance with specialized laws on education and training, health and other socialized fields; undivided incomes for forming assets of cooperatives which are established and operate in accordance with the Law on Cooperatives.

11. Incomes from technology transfer in the fields in which technology transfer to organizations and individuals in localities with particularly difficult socio-economic conditions is prioritized.

Chapter II . TAX BASES AND TAX CALCULATION METHODS

Article 5. Tax bases

Tax bases include taxed income in a tax period and tax rate.

Tax period is specified in Article 5 of the Law on Enterprise Income Tax and the law on tax administration.

Enterprises may choose to apply a tax period according to the calendar year or fiscal year but shall register it with tax agencies before application.

Article 6. Determination of taxed incomes

1. Taxed income in a tax period shall be determined as follows:

Taxed income = Taxable income – (Tax-exempt income + Losses carried forward under regulations)

2. Taxable income shall be determined as follows:

Taxable income = (Turnover – Deductible expenses) + other incomes

For an enterprise conducting different business activities, taxable income from production and business activities is the total of incomes from all business activities. If a business activity makes losses, the enterprise may offset such losses with the taxable income of an income-generating business activity selected by the enterprise. The remaining income after loss offsetting is subject to the rate of enterprise income tax on income-generating business activities.

Incomes from the transfer of real estate, transfer of investment projects, transfer of the right to join investment projects, transfer of mineral exploration, exploitation or processing right must be separately accounted for tax declaration and payment. In case the transfer of the right to join investment projects or transfer of investment projects (except projects on mineral exploration or exploitation) or transfer of real estate makes losses, such losses may be offset with profits of production and business activities in a tax period. In case an enterprise carrying out dissolution procedures sells real estate being fixed assets, income (if any) from transfer of real estate may be offset with income from production and business activities of the enterprise.

3. Taxable incomes from some production and business activities shall be determined as follows:

a/ For income from capital transfer (excluding income from securities transfer specified at Point b of this Clause), taxable income is the total money amount collected under the transfer contract minus (-) the purchase price of the transferred capital amount, minus (-) expenses for the transfer.

An enterprise that transfers capital not in cash but in asset or other material benefits (stocks or fund certificates) and earns incomes shall pay enterprise income tax;

b/ For income from securities transfer, taxable income is the selling price minus (-) the purchase price of the transferred securities, minus (-) expenses for the transfer.

For an enterprise that issues stocks, the difference between the issuance price and the par value of stocks is not liable to enterprise income tax.

For an enterprise undergoing separation, split, consolidation or merger that swaps stocks at the time of separation, split, consolidation or merger and earns income, such income is liable to enterprise income tax.

An enterprise that transfers securities not in cash but in asset or other material benefits (stocks or fund certificates) and earns incomes shall pay enterprise income tax;

c/ For income from intellectual property rights or technology transfer, taxable income is the total collected money amount minus (-) the cost or expense for creating the transferred intellectual property right or technology, minus (-) the expense for maintaining, upgrading or developing the transferred intellectual property right or technology, and other deductible expenses;

d/ For income from asset lease, taxable income is the lease turnover minus (-) basic depreciation, expense for asset renovation, repair and maintenance, expense for lease of assets for sublease (if any) and other deductible expenses related to the lease;

dd/ For income from the transfer or liquidation of assets (except real estate), taxable income is the money amount collected from asset transfer or liquidation minus (-) the residual book value of assets at the time of transfer or liquidation and deductible expenses related to the transfer or liquidation;

e/ For income from foreign currency sales, taxable income is the total money amount collected from foreign currency sales minus (-) the cost price of the quantity of sold foreign currencies;

g/ For difference resulting from the revaluation of assets transferred upon the separation, split, consolidation, merger, transformation of enterprises, change of owners or capital contribution, taxable income is the difference between the revaluated value and the residual book value of such assets before the revaluation.

The positive or negative difference resulting from the revaluation of fixed assets for capital contribution, assets transferred upon the separation, split, consolidation, merger or transformation of enterprises, or assets being the value of the land use rights contributed as capital to investment projects on construction of houses and infrastructure facilities for sale, may be accounted as other incomes or reductions of other incomes in a tax period; particularly, the difference resulting from the revaluation of land use rights contributed as capital which capital contribution recipients may not depreciate may be incrementally accounted as other incomes for not more than 10 years;

h/ For business cooperation contracts (BCC) which divide after-tax profits, income is the total turnover generated under such contracts minus (-) total expenses related to the generation of turnover under such contracts.

The Ministry of Finance shall specifically guide the determination of turnover and expenses of BCC which divide after-tax profits;

i/ For incomes received from overseas production and business activities, taxable income is the total of pre-tax incomes.

4. Incomes from oil and gas exploration and extraction are determined based on each oil and gas contract.

Article 7. Determination and carrying forward of losses

1. Loss arising in a tax period is the negative (-) taxable income amount exclusive of losses carried forward from previous years and determined according to the formula specified in Clause 1, Article 6 of this Decree.

2. Loss-suffering enterprises may carry forward their losses to the subsequent year; these losses may be offset with taxable incomes. The maximum duration for carrying forward losses is 5 consecutive years, counting from the year following the year the losses arise.

3. Losses from transfer of real estate, investment projects or the right to join investment projects (except mineral exploration and exploitation projects) remaining after being offset with taxable incomes of this activity or offset under Clause 2, Article 6 of this Decree and losses from transfer of mineral exploration and exploitation rights may be carried forward to the subsequent year as taxable incomes of such activity. The maximum duration for carrying forward losses is 5 consecutive years, counting from the year following the year the losses arise.

Article 8. Turnover

Turnover used for calculating taxable income is specified in Article 8 of the Law on Enterprise Income Tax.

1. Turnover used for calculating taxable income is the total of sales, processing remunerations and service charges, including also subsidies and surcharges enjoyed by enterprises, regardless of whether money has been collected or not.

For enterprises declaring and paying value-added tax by the tax credit method, turnover used for calculating enterprise income tax is exclusive of value-added tax. For enterprises declaring and paying value-added tax by the method of calculation of tax based directly on added value, turnover used for calculating enterprise income tax is inclusive of value-added tax.

2. The time of determining turnover used for calculating taxable income for goods sold is the time of transfer of the right to own or use goods to purchasers.

The time of determining turnover used for calculating taxable income for services is the time of completing the provision of services to purchasers or the time of making service provision invoices.

3. Turnover used for calculating taxable income in some cases is specified as follows:

a/ For goods sold on installment payment, it is determined based on the lump-sum selling price, excluding installment or deferred payment interests;

b/ For goods and services used for barter or internal consumption (excluding goods and services used for sustaining the production and business of enterprises), it is determined based on the selling price of products, goods or services of the same or similar categories at the time of barter or internal consumption;

c/ For goods processing activities, it is the proceeds from processing activities, including remuneration, expenses for fuel, power and auxiliary materials, and other expenses for the processing;

d/ For asset lease, golf course business or other services for which customers pay rent or charge in advance for many years, it is the rent amount paid periodically by lessees or service purchasers under contracts. In case lessees or service purchasers advances the rent for many years, it is allocated to the number of years for which the rent has been advanced, or be determined according to the turnover paid in lump sum. For enterprises currently enjoying tax incentives, tax amounts eligible for incentives must be determined based on the total payable enterprise income tax amount of the years for which the rent is advanced divided by the number of years;

dd/ For credit or financial leasing activities, it is the receivable loan interest or financial lease turnover arising in a tax period;

e/ For transportation activities, it is the whole turnover from passenger fares and cargo and luggage freights arising in a tax period;

g/ For electricity and clean water supply activities, it is the money amount indicated on the value-added invoice;

h/ For insurance or reinsurance business activities, it is the receivable amount of principal insurance premiums; agency service charges (including those for loss survey, indemnity consideration, claim for a third party to pay indemnities, disposal of goods subject to 100% indemnity); reinsurance undertaking charges; reinsurance commissions, and other insurance business revenues minus (-) refunded or reduced insurance premiums, reinsurance undertaking charges and refunded or reduced reinsurance receding commissions.

In case of co-insurance, turnover used for calculating taxable income is principal insurance premiums allocated according to the co-insurance ratio, exclusive of value-added tax.

For insurance policies containing an agreement on periodical payment of premiums, it is the receivable money amount arising in each period;

i/ For construction and installation activities, it is the value of the work, work item or work volume subject to takeover test.

If construction or installation activities do not involve the supply of materials, machinery and equipment, it is exclusive of the value of materials, machinery or equipment;

k/ For business activities conducted under business cooperation contracts without the establishment of legal persons:

– If parties to a business cooperation contract divide business results based on the sales turnover of goods or services, it is the turnover divided to each party under the contract;

– If parties to a business cooperation contract divide business results based on pre-tax profits, it is the goods or service sales under the contract;

l/ For casino, prize-winning video game or betting entertainment business services, it is the excise tax-inclusive proceeds from these services minus (-) prizes already paid to customers;

m/ For securities trading, it is the proceeds from securities brokerage, dealing, issuance underwriting and investment consultancy, investment fund management, fund certificate issuance, market organization and other securities services in accordance with law;

n/ For oil and gas prospecting, exploration and extraction activities, it is the whole oil and gas sales turnover under arm’s length contracts in a tax period;

o/ For derivative financial services, it is the proceeds from the provision of derivative financial services in a tax period;

The Ministry of Finance shall specifically guide this Article and some other specific cases.

Article 9. Deductible and non-deductible expenses upon determination of taxable incomes

1. Except for the expenses specified in Clause 2 of this Article, enterprises may deduct any expenses which fully satisfy the following conditions:

a/ They are actually paid for production and business activities of enterprises, including the following expenses:

– Expense for the performance of the task of national defense and security education, drills and operation of militia and self-defense forces and other national defense and security tasks in accordance with law; expense for operations of Party organizations and socio-political organizations in enterprises;

– Expenses actually paid for HIV/AIDS prevention and control at workplaces of enterprises, including expense for training of HIV/AIDS prevention and control personnel of enterprises, expense for HIV/AIDS communication among employees of enterprises, charges for medical consultation, examination and HIV test, expense for HIV-infected employees of enterprises.

b/ They have adequate invoices and documents as prescribed by law.

In case of purchase of agricultural, forestry or fishery products from producers or fishermen; purchase of handicraft products made of jute, sedge, bamboo, leaf, rattan, straw, coconut husk or shell or materials taken from agricultural products, from craftsmen; purchase of soil, rock, sand or gravel from local mining households or individuals; purchase of scraps from individual collectors or second-hand domestic appliances and assets from households or individuals, and purchase of services from non-business households or individuals, there must be documents of payment to sellers and a list of goods or services signed by at-law representatives or authorized persons of enterprises;

c/ For one-off purchase invoices of goods or services which are valued at VND 20 million or more, there must be documents of non-cash payment, excluding expenses paid by enterprises for the performance of the national defense and security task, HIV/AIDS prevention and control at workplaces, expense for operations of Party organizations and socio-political organizations in enterprises as specified at Point a, Clause 1 of this Article; expense for the purchase of goods and services specified at Point b, Clause 1 of this Article for which a list may be made.

The Ministry of Finance shall specifically guide the case in which payments under contracts are made and recorded at different points of time and other expenses not required to have non-cash payment documents.

2. Non-deductible expenses upon the determination of taxable incomes under Clause 2, Article 9 of the Law on Enterprise Income Tax and Clause 5, Article 1 of the Law Amending and Supplementing a Number of Articles, are specified as follows:

a/ Expenses which do not fully satisfy the conditions specified in Clause 1 of this Article, except the uncompensated value of losses caused by natural disasters, epidemics, fires or other force majeure circumstances;

Uncompensated value of losses caused by natural disasters, epidemics, fires or other force majeure circumstances is the total value of losses minus (-) the value which must be compensated by insurance enterprises or other organizations or individuals in accordance with law;

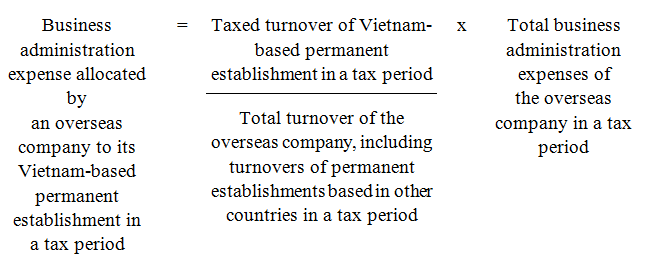

b/ The business administration expense allocated by an overseas enterprise to its Vietnam-based permanent establishment in excess of the prescribed level is calculated according to the following formula:

c/ Expense in excess of the prescribed level of deduction for the setting up of provisions;

d/ Fixed asset depreciation made in contravention of the Finance Ministry’s regulations, including depreciation for passenger cars of 9 seats or less (except cars used for commercial transportation of passengers or for tourist or hotel business) corresponding to the historical cost in excess of VND 1.6 billion/car; depreciation for civil aircraft or yachts not used for commercial cargo or passenger transportation or for tourist or hotel business;

dd/ Advanced expenses in contravention of law.

Advanced deductible expenses include those for regular overhaul of fixed assets; those for activities of which turnover has been accounted but contractual obligations have not yet been fulfilled, including the case of asset lease with advance payment of rent for many years in which the lessor accounts the whole paid rent into the turnover of the year of rent collection; and other advanced expenses under the Finance Ministry’s regulations;

e/ Loan interests paid corresponding to insufficient charter capital amount to be contributed according to the schedule indicated in the enterprise’s charter; loan interests recorded as asset value; interests on loans for the performance of oil and gas prospecting, exploration and exploitation contracts;

g/ Expense for advertising, marketing, sales promotion and brokerage commissions (excluding insurance brokerage commissions under the law on insurance business or commissions for agents selling goods at set prices, commissions for distributors of multi-level marketing businesses); expense for guest reception, protocol and conferences; expense in support of marketing and activities directly related to production and business activities, in excess of 15% of total deductible expenses.

Total deductible expenses exclude the expenses specified above; for commercial activities, total deductible expenses exclude purchase prices of goods sold.

Expenses subject to expenditure limitations specified at this Point include also gifts, presents and donations given to customers.

h/ Expenses allowed to be recovered in excess of the ratio set in approved oil and gas contracts; if an oil and gas contract does not set the ratio of recoverable expenses, the expense in excess of 35% must not be included in deductible expenses; expenses which may not be included in recoverable expenses include:

– Expenses specified in Clause 2, Article 9 of the Law on Enterprise Income Tax and at Point 2, Clause 5, Article 1 of the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax;

– Expenses arising before oil and gas contracts come into force, except those agreed under oil and gas contracts or decided by the Prime Minister;

– Various oil and gas commissions and other expenses not included in recoverable expenses under contracts;

– Interests on investments in prospecting, exploration and development of oil and gas fields and oil and gas exploitation;

– Fines and damages.

i/ Credited input value-added tax, uncredited input value-added tax on the value of under-9-seat cars in excess of VND 1.6 billion, enterprise income tax and other taxes, charges, fees and revenues not allowed to be accounted as expenses under the Finance Ministry’s regulations;

k/ Expenses not corresponding to taxed turnover, except a number of special cases as guided by the Ministry of Finance;

l/ Foreign exchange rate difference resulting from the revaluation of monetary items of foreign currency origin at the end of a tax period, except foreign exchange rate difference resulting from the revaluation of payable debts of foreign currency origin at the end of the tax period, and exchange rate difference arising in the course of capital construction investment to form fixed assets of newly established enterprises which are not yet put into production or business comply with the guidance of the Ministry of Finance.

For receivable debts and loans of foreign currency origin provided in the period, foreign exchange rate difference allowed to be accounted as a deductible expense is the difference between the exchange rate at the time of debt or loan recovery and the exchange rate at the time of recording receivable debts or initial loans;

m/ Salaries or wages of owners of private enterprises, owners of single-member limited liability companies (owned by individuals); remunerations paid to enterprise founders who do not personally participate in administering production and business activities; salaries, wages and other amounts accounted as expenses payable to employees which have actually not been paid or have been paid without invoices or documents as prescribed by law; bonuses and expenses for purchase of life insurance for employees for which the payment conditions and levels are not specified in any of the following papers: labor contracts; collective labor agreements; financial regulations of companies, corporations or groups; or reward regulations issued by chairpersons of Boards of Directors, directors general or directors under financial regulations of companies or corporations. Salaries or wages and allowances payable to employees which are not actually paid upon the expiration of the time limit for submission of annual tax finalization dossiers, except where the enterprise sets aside provisions to be added to the salary fund of the subsequent year in order to ensure that the salary payment is uninterrupted and the fund is not used for other purposes. The annual provision level may be decided by the enterprise but must not exceed 17% of the actual salary fund (the total salary amount actually paid in the year of tax finalization by the deadline for submission of the finalization dossier and exclusive of the salary provision set aside in the previous year and used in the year of tax finalization). In case the salary provision set aside by the enterprise in the previous year remains unused or is not used up within 6 months after the end of the fiscal year, the enterprise shall record it as a reduction of expenses in the subsequent year;

n/ Financial aid, except aid for education, health, scientific research, remediation of consequences of natural disasters, building of great solidarity or gratitude houses or houses for the poor and policy beneficiaries in accordance with law, aid under the State’s programs for localities with particularly difficult socio-economic conditions.

Institutions receiving aid for scientific research specified at this Point are scientific and technological institutions established and operating in accordance with the Law on Science and Technology and performing science and technology tasks in accordance with the law on science and technology.

o/ Expense in excess of the level of VND 1 million/month/person for setting up the voluntary pension fund or purchasing voluntary retirement insurance and life insurance for employees; expense in excess of the level prescribed by the laws on social insurance and health insurance for setting up funds of social security nature (compulsory social insurance and retirement insurance), health insurance fund and unemployment insurance fund for employees.

Deductions for payment of contributions to the voluntary pension fund and funds of social security nature or for purchase of voluntary retirement insurance and life insurance for employees may be accounted as deductible expenses and must not exceed the level specified in this Clause while conditions for receipt of and level of insurance sums must be specified in any of the following dossiers: labor contracts, collective labor agreements, financial regulations of companies, corporations or groups; reward regulations set out by chairpersons of Boards of Directors, directors general or directors in accordance with financial regulations of companies or corporations;

p/ Expenses for banking, insurance, lottery and securities business and some other special business activities as prescribed by the Ministry of Finance;

q/ Late-tax payment interests as prescribed by the Law on Tax Administration;

r/ Expense directly related to the issuance of stocks (except stocks in the form of payable debt) and stock dividends (except dividends of stocks in the form of payable debts), purchase and sale of fund stocks and other expenses directly related to the increase or reduction of equity capital of enterprises.

The Ministry of Finance shall specifically guide deductible and non-deductible expenses specified in this Article.

Article 10. Tax rates

Enterprise income tax rates are specified in Clause 6, Article 1 of the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax:

1. The enterprise income tax rate is 22%, except the cases in which enterprises are subject to the tax rate of 20% and the tax rate of between 32% and 50% specified in Clauses 2 and 3 of this Article and those eligible for tax rate incentives specified in Articles 15 and 16 of this Decree.

From January 1, 2016, enterprises subject to the tax rate of 22% specified in this Clause will be subject to the tax rate of 20%.

2. Enterprises established and operating in accordance with Vietnamese law, including cooperatives and non-business units engaged in goods production and trading or service provision and having an annual total turnover of VND 20 billion or less is subject to the tax rate of 20%.

The annual total turnover serving as a ground for identifying an enterprise subject to the tax rate of 20% specified in this Clause is the total turnover from goods sale or service provision of such enterprise in the previous year.

3. The enterprise income tax rate applicable to activities of prospecting, exploring and exploiting oil and gas and other precious and rare natural resources in Vietnam is between 32% and 50%. Based on the location, exploitation conditions and reserves of mines, the Prime Minister shall, at the proposal of the Minister of Finance, decide on a specific tax rate applicable to each project or business establishment. Mines of mineral resources of platinum, gold, silver, tin, tungsten, antimony, gems and rare earths are subject to the tax rate of 50%. Mines with 70% or more of their assigned areas in localities with particularly difficult socio-economic conditions on the list of localities eligible for enterprise income tax incentives promulgated together with this Decree are subject to the tax rate of 40%.

Article 11. Tax calculation method

1. An enterprise income tax amount payable in a tax period is equal to taxed income multiplied by (x) the tax rate; in case an enterprise has paid income tax on incomes arising overseas, the paid tax amount may be subtracted but must not exceed the enterprise income tax amount payable under the Law on Enterprise Income Tax.

2. The payable enterprise income tax amount applicable to real estate transfer is income from real estate transfer multiplied by (x) the tax rate of 22%, or 20% from January 1, 2016.

3. For enterprises defined at Points c and d, Clause 2, Article 2 of the Law on Enterprise Income Tax, the payable enterprise income tax amount is the percentage (%) of the sales turnover of goods and services in Vietnam, specifically:

a/ Services: 5%, particularly restaurant, hotel and casino management services: 10%; services provided together with goods: 1%; services provided in case it is impossible to separate the goods value from the service value: 2%;

b/ Provision and distribution of goods in Vietnam in the form of on-the-spot import and export or under the international commercial terms: 1%;

c/ Copyright royalties: 10%;

d/ Charter of aircraft (including aircraft engines or spare parts) or seagoing ships: 2%;

dd/ Hire of drilling platforms, machinery, equipment or means of transport (except those specified at Point d of this Clause): 5%;

e/ Loan interests: 5%;

g/ Securities transfer and overseas ceding of reinsurance: 0.1%;

h/ Derivative financial services: 2%;

i/ Construction, transportation and other activities: 2%.

4. For oil and gas exploitation under contracts indicating the accounting of turnover and expenditures in a foreign currency, taxed income and payable tax amount must be calculated in such foreign currency.

5. Non-business units and organizations other than enterprises established and operating in accordance with Vietnamese law which are engaged in goods trading or service provision, earn incomes liable to enterprise income tax and can account their turnover but cannot account expenditures and incomes of their business activities shall declare and pay enterprise income tax at a percentage (%) of turnover from goods or service sale, specifically as follows:

a/ For services (including deposit and loan interests): 5%. Particularly, educational, health care and art performance activities are subject to the tax rate specified at Point c of this Clause;

b/ For goods trading: 1%;

c/ For other activities: 2%.

Article 12. Places for tax payment

1. Enterprises shall pay tax in localities where they are headquartered. For an enterprise that has a dependent cost-accounting production establishment operating in a province or centrally run city other than the locality where it is headquartered, the tax amount must be calculated and paid in the locality where the enterprise is headquartered and the locality where its production establishment is based.

The enterprise income tax amount calculated and paid in a province or centrally run city where the dependent cost-accounting production establishment is based is the enterprise income tax amount payable by the enterprise in a period multiplied by (x) the ratio of expenses arising in the production establishment to the total expenses of the enterprise.

Tax payment specified in this Clause is not applicable to works, work items or dependent cost-accounting construction establishments.

The decentralization, management and use of enterprise income tax revenues comply with the Law on the State Budget.

2. Dependent cost-accounting units of enterprises practicing cost-accounting in the whole system that have incomes from activities other than their core business lines shall pay tax in provinces or centrally run cities where other activities are carried out.

3. The Ministry of Finance shall guide places for tax payment mentioned in this Article.

Chapter III. INCOMES FROM REAL ESTATE TRANSFER

Article 13. Incomes from real estate transfer include income from the transfer of land use or lease rights; income from sublease of land of real estate-trading enterprises in accordance with the land law, regardless of whether infrastructure or architectural works attached to land are available or not; income from the transfer of houses or construction works attached to land, including assets attached to such houses or construction works, regardless of whether land use or lease rights are transferred or not; and income from the transfer of other assets attached to land.

1. Turnover used for calculating taxable income shall be determined based on the real price of real estate transfer under real estate purchase and sale contracts in accordance with law.

If the price of transfer of land use rights under a real estate purchase and sale contract is lower than the land price set by the provincial-level People’s Committee at the time of contract signing, the price set by the provincial-level People’s Committee shall be applied.

2. The time of determining turnover used for calculating taxable income is the time of handover of real estate.

If money is advanced according to schedule, the time of determining turnover used for calculating the enterprise income tax amount to be temporarily paid is the time of money collection. The Ministry of Finance shall guide the temporary tax payment referred to this Clause.

3. Deductible expenses for real estate transfer:

a/ The cost price of transferred land, to be determined according to the origin of land use rights, specifically:

– For land allocated by the State with land use levy or land rent, its cost price is the land use levy or lease rent actually remitted into the state budget;

– For land transferred from other organizations or individuals, its cost price is based on contracts and lawful payment documents upon the receipt of land use or lease rights; if contracts and lawful payment documents are unavailable, such cost price must be calculated based on the price set by the provincial-level People’s Committee at the time the enterprise receives real estate transferred;

– For land contributed as capital, its cost price is the price agreed upon capital contribution;

– For inherited or donated land with unidentifiable cost price, such cost price must be determined based on the land price set by the provincial-level People’s Committee at the time of inheritance or donation.

For land inherited or donated before 1994, its cost price must be determined based on the land prices set in 1994 by the provincial-level People’s Committee on the basis of the Table of land price brackets in the Government’s Decree No. 87/CP of August 17, 1994;

b/ Expense for compensations and support upon land recovery by the State;

c/ Charges and fees related to the grant of land use rights in accordance with law;

d/ Expense for soil improvement or ground fill-up and leveling;

dd/ Value of infrastructure or architectural works on land;

e/ Other expenses related to transferred real estate.

Chapter IV. ENTERPRISE INCOME TAX INCENTIVES

Article 15. Tax rate incentives

1. The preferential tax rate of 10% for 15 years is applicable to:

a/ Incomes earned by enterprises from the implementation of new investment projects in localities with particularly difficult socio-economic conditions specified in the Appendix to this Decree, economic zones and hi-tech parks, including information technology parks established under the Prime Minister’s decisions;

b/ Incomes earned by enterprises from the implementation of new investment projects in the fields of scientific research and technology development; application of high technologies on the list of high technologies prioritized for development investment in accordance with the Law on High Technology; incubation of high technologies and hi-tech enterprises; venture investment for development of high technologies on the list of high technologies prioritized for development investment in accordance with the Law on High Technology; investment in construction and commercial operation of high technology and high technology enterprise incubation; investment in development of water plants, power plants, water supply and drainage systems; bridges, roads, railways; airports, seaports, river ports; airfields, stations and other infrastructure works of special importance as decided by the Prime Minister; manufacture of software products; manufacture of composite materials, light building materials and precious and rare materials; generation of renewable energy, clean energy and energy from the disposal of waste; development of bio-technology.

Investment projects on manufacture of software products specified at this Point are those on manufacture of software products on the list of software products and applying the law-prescribed process of manufacture of software products;

c/ Incomes earned by enterprises from the implementation of new investment projects in the field of environmental protection, covering manufacture of equipment for treatment of environmental pollution and equipment for environmental observation and analysis; environmental pollution treatment and environmental protection; collection and treatment of wastewater, exhaust gas and solid waste; recycling and reuse of waste;

d/ Incomes earned by hi-tech enterprises and agricultural enterprises applying high technologies

In case enterprises currently enjoying enterprise income tax incentives or have enjoyed all enterprise income tax incentives under legal documents on enterprise income tax are granted certificates of hi-tech enterprises or agricultural enterprises applying high technologies, the incentive levels for such enterprises are equal to that applicable to hi-tech enterprises and agricultural enterprises applying high technologies specified in Clause 1, Article 15 and Clause 1, Article 16 of this Decree minus the enjoyed incentives (including tax rate incentives and exemption or reduction, if any);

dd/ Incomes earned by enterprises from the implementation of new investment projects in the field of production (except projects on production of goods liable to excise tax and mineral mining projects) which satisfy either of the following criteria:

– Being capitalized at least VND 6 trillion, having their capital disbursed within 3 years from the date of grant of investment licenses, and earning a total turnover of at least VND 10 trillion/year within 3 years from the date of earning turnover.

– Being capitalized at least VND 6 trillion, having their capital disbursed within 3 years from the date of grant of investment licenses, and employing more than 3,000 laborers within 3 years from the date of earning turnover.

Laborers specified at this Point are those signing labor contracts to work on a full-time basis, excluding those working on a part-time basis or under labor contracts of a term of under 1 year.

2. The tax rate of 10% is applicable to the following incomes:

a/ Incomes earned by enterprises from their socialized education-training, vocational training, health care, cultural, sports and environmental protection activities.

The list of types, size and standards of enterprises engaged in socialized fields mentioned in this Clause is promulgated by the Prime Minister.

b/ Incomes from publication activities of publishing houses in accordance with the Law on Publication;

c/ Incomes from print newspapers (including advertising on print newspapers) of press agencies in accordance with the Law on Press;

d/ Incomes from earned by enterprises from the implementation of investment projects on social houses for sale, lease or hire-purchase to the subjects specified in Article 53 of the Housing Law.

Social houses specified in this Clause are houses built by the State or organizations or individuals of all economic sectors and satisfying the criteria for houses, house prices, rent rates, hire-purchase prices, eligible subjects, conditions on purchase, rent or hire-purchase of social houses in accordance with the housing law, and the determination of incomes subject to the tax rate of 10% specified in this Clause does not depend on the time of signing of social house sale, lease or hire-purchase contracts;

dd/ Incomes earned by enterprises from cultivation, tending and protection of forests; planting or rearing agricultural, forest or aquatic products in localities with difficult socio-economic conditions; production, propagation and cross-breeding of plant varieties and animal breeds; production, exploitation and purification of salt, except salt production specified in Clause 1, Article 4 of this Decree; post-harvest preservation of agricultural products or preservation of agricultural and aquatic products and foods;

e/ Incomes of cooperatives operating in agriculture, forestry, fisheries or salt production and not located in localities with difficult socio-economic conditions or those with particularly difficult socio-economic conditions, except incomes of cooperatives specified in Clause 1, Article 4 of this Decree.

3. The tax rate of 20% for 10 years is applicable to:

a/ Incomes earned by enterprises from the implementation of new investment projects in localities with difficult socio-economic conditions specified in the Appendix to this Decree.

b/ Incomes earned by enterprises from the implementation of new investment projects on manufacture of hi-grade steel, energy-saving products, machinery and equipment for agricultural production, forestry, fisheries or salt production, irrigation and drainage equipment; production or processing of cattle, poultry or aquatic animal feed; or development of traditional crafts or trades.

From January 1, 2016, enterprises implementing new investment projects in the fields or localities eligible for tax incentives specified at Points a and b of this Clause will be subject to the tax rate of 17%.

4. The tax rate of 20% is applicable to people’s credit funds and microfinance institutions, which will be subject to the tax rate of 17% from January 1, 2016.

Upon the expiration of the duration of application of the tax rate of 10% specified in Clause 1 of this Article, people’s credit funds and microfinance institutions shall switch to be subject to the tax rate of 20% (or 17% from January 1, 2016). Microfinance institutions specified in this Clause are those established and operating in accordance with the Law on Credit Institutions.

5. For large-sized and hi-tech or new projects eligible for tax incentives specified at Points b and c, Clause 1 of this Article in which investment needs to be specially attracted, the duration of application of the preferential tax rate of 10% may be prolonged but must not exceed 30 years. The Prime Minister shall decide to prolong the duration of application of the preferential tax rate of 10% specified in this Clause at the request of the Minister of Finance.

6. The duration of application of the preferential tax rate specified in this Article shall be counted consecutively from the first year of earning turnover from new investment projects; for hi-tech enterprises and agricultural enterprises applying high technologies, the duration shall be counted from the date these enterprises are recognized as hi-tech enterprises or agricultural enterprises applying high technologies; for projects applying high technologies, the duration shall be counted from the date of grant of certificates of projects applying high technologies.

Article 16. Tax exemption and reduction

1. Tax exemption for 4 years and 50% reduction of payable tax amounts for 9 subsequent years are applicable to:

a/ Incomes earned by enterprises from the implementation of new investment projects specified in Clause 1, Article 15 of this Decree;

b/ Incomes earned by enterprises from the implementation of new investment projects in the socialized fields in localities with difficult socio-economic conditions or particularly difficult socio-economic conditions specified in the Appendix to this Decree.

2. Tax exemption for 4 years and 50% reduction of payable tax amounts for 5 subsequent years are applicable to incomes earned by enterprises from the implementation of new investment projects in the socialized fields in localities not on the list of localities with difficult socio-economic conditions or particularly difficult socio-economic conditions specified in the Appendix to this Decree.

3. Tax exemption for 2 years and 50% reduction of payable tax amounts for 4 subsequent years are applicable to incomes earned by enterprises from the implementation of new investment projects specified in Clause 3, Article 15 of this Decree and new investment projects in industrial parks (except those in localities with favorable socio-economic conditions).

Localities with favorable socio-economic conditions specified in this Clause are inner districts of centrally run special-grade or grade-I urban centers and provincially run grade-I urban centers; the determination of tax incentives for industrial parks located in both localities with favorable and unfavorable conditions must be based on localities with larger areas of these industrial parks. The determination of special-grade or grade-I urban centers specified in this Clause must comply with regulations of the Government on classification of urban centers.

4. The tax exemption or reduction duration specified in this Article is counted consecutively from the first year an enterprise has taxable income from a new investment project eligible for tax incentives; in case an enterprise has no taxable income during the first 3 years, counting from the first year it has turnover from a new investment project, the tax exemption or reduction duration shall be counted from the fourth year. The tax exemption or reduction duration for hi-tech enterprises and agricultural enterprises applying high technologies specified in Clause 1 of this Article shall be counted from the time these enterprises are recognized as hi-tech enterprises or agricultural enterprises applying high technologies.

In the first tax period, if the new investment project of an enterprise with a production and business duration eligible for tax exemption or reduction of under 12 (twelve) months, the enterprise may choose to enjoy the tax exemption or reduction for the new investment project right in such tax period or register with the tax agency the time of starting to enjoy the tax exemption or reduction from the subsequent tax period.

5. Enterprises that have development investment projects or operating investment projects in the fields or localities eligible for enterprise income tax incentives under this Decree which expand their production, increase their productivity or renew their production technologies and satisfy one of the three criteria specified in this Clause may choose to enjoy the tax incentives under operating projects for the remaining duration (if any) or enjoy the tax exemption or reduction for additional incomes brought about by expanded investment. The tax exemption or reduction duration for additional incomes brought about by expanded investment specified in this Clause equals that applicable to new investment projects in the same localities or fields eligible for enterprise income tax incentives.

An expanded investment project specified in this Clause must satisfy one of the following criteria:

– The historical cost of additional fixed assets upon its completion and commissioning is at least VND 20 billion, for projects in the fields eligible for the enterprise income tax incentives specified in this Decree, or at least VND 10 billion, for projects implemented in localities with difficult socio-economic conditions or particularly difficult socio-economic conditions in accordance with the law on enterprise income tax;

– The ratio of the historical cost of additional fixed assets equals at least 20% of the total cost of fixed assets before investment;

– The design capacity increases at least 20% after investment.

In case an operating enterprise invests in upgrading, replacement or renewal of technology of an operating project in a field or locality eligible for the tax incentives under this Decree but fails to satisfy one of the three criteria specified at this Point, the tax incentives will be granted to the operating project for the remaining duration (if any).

In case an enterprise chooses to enjoy the tax incentives for expanded investment, the additional income brought about by expanded investment must be separately accounted; in case it is impossible to separately account such income, it shall be determined according to the ratio of the historical cost of fixed assets used for production or business activities to the total costs of fixed assets of the enterprise.

The tax exemption or reduction duration specified in this Clause shall be counted from the year when the expanded investment project is completed and put into production or business and earns income; in case no taxable income is earned in the first 3 years from the year of generation of turnover from the expanded investment project, the tax exemption or reduction duration shall be counted from the fourth year.

The tax incentives specified in this Clause are not applicable to cases of expanded investment from merger and acquisition of operating enterprises or investment projects.

Article 17. Tax reduction in other cases

1. Production, construction or transport enterprises which employ between 10 and 100 female laborers who account for more than 50% of their total regular employees or regularly employ over 100 female laborers who account for more than 30% of their total regular employees are entitled to reduction of enterprise income tax amounts equal to additional expenses paid for female laborers, including:

a/ Expense for job retraining;

b/ Salaries and allowances (if any) for teachers in crèches and kindergartens organized and managed by the enterprises;

c/ Expense for additional health check-ups in a year;

d/ Post-natal allowances for female laborers. The Ministry of Finance shall, pursuant to the labor law, coordinate with the Ministry of Labor, War Invalids and Social Affairs in specifying post-natal allowance levels mentioned in this Clause;

dd/ Salaries and allowances for female laborers who return to work while still on prescribed maternity leave.

2. Enterprises that employ ethnic minority laborers are entitled to reduction of enterprise income tax amounts equal to additional expenses for job training, housing subsidies, social insurance premiums and health insurance premiums for these laborers, if they have not yet received the State’s supports under regulations.

3. Enterprises that transfer technologies in the fields prioritized for technology transfer to organizations or individuals in localities with difficult socio-economic conditions are entitled to 50% reduction of enterprise income tax on the income from technology transfer.

Article 18. Deduction for setting up science and technology development funds of enterprises

The deduction for setting up science and technology development funds of enterprises complies with Article 17 of the Law on Enterprise Income Tax and Clause 11, Article 1 of the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax.

1. Enterprises established and operating under Vietnamese law may deduct up to 10% of annual taxed income for setting up their science and technology development funds. Particularly, enterprises of which the State holds more than 50% of charter capital, in addition to making deduction for setting up the science and technology development funds under this Law, they shall ensure the minimum deduction level for setting up the funds as prescribed in the Science and Technology Law.

Annually, enterprises may decide by themselves on the level of deduction for setting up their science and technology development funds under the above provision and make reports on the setting up and use of such funds, enclosed with enterprise income tax finalization declarations.

The Ministry of Finance shall issue the form of report on the setting up and use of the science and technology development fund of enterprises.

2. For operating enterprises which undergo ownership transformation, are consolidated or merged, the new enterprises set up as a result of such ownership transformation, consolidation or merger may take over the science and technology development funds of the former enterprises and shall take responsibility for the management and use of such funds.

If the science and technology development fund of an enterprise is not used up upon its separation or split, the new enterprise set up as a result of such separation or split may take over the science and technology development fund of the former enterprise and shall take responsibility for the management and use of such fund. Enterprises shall decide on and register with tax agencies the division of their science and technology development funds.

Article 19. Conditions for application of enterprise income tax incentives

Conditions for application of enterprise income tax incentives are specified in Clause 12, Article 1 of the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax.

1. Enterprises shall separately account income from production and business activities eligible for enterprise income tax incentives (including preferential tax rates or tax exemption or reduction); any turnover or deductible expenses which cannot be separately accounted must be determined based on the ratio of deductible expenses or turnover from production and business activities eligible for tax incentives to the total deductible expenses or turnover of enterprises.

2. The enterprise income tax incentives specified in Clauses 1 and 4, Article 4 and Articles 15 and 16 of this Decree and the tax rate of 20% specified in Clause 2, Article 10 of this Decree are not applicable to:

a/ Income from the transfer of capital or the capital contribution right; income from the transfer of real estate, except income from investment and commercial operation of social houses specified at Point d, Clause 2, Article 15 of this Decree; income from the transfer of investment projects, the right to join investment projects or the mineral exploration or exploitation right; and income earned from production or business activities outside Vietnam;

b/ Income from the prospecting, exploration or exploitation of oil, gas and other precious and rare natural resources and income from mineral mining;

c/ Income from the provision of services liable to excise tax in accordance with the Law on Excise Tax;

d/ Other incomes specified in Clause 2, Article 3 of this Decree not earned from production or business activities eligible for tax incentives (for fields or sectors eligible for the incentives specified in Articles 15 and 16 of this Decree).

3. In the same duration, an enterprise which is entitled to different tax incentives for the same income may choose to apply the highest incentive.

4. In a tax year within the duration of enjoyment of the enterprise income tax incentives, if an enterprise fails to satisfy one of the conditions for enjoyment of the tax incentives specified in Clauses 7, 8 and 12, Article 1 of the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax and this Article, it is not entitled to the tax incentives in such tax year and shall pay tax at the rate of 22%, or of 20% for enterprises with a total annual turnover of VND 20 billion or less specified in Clause 2, Article 10 of this Decree. From January 1, 2016, the common tax rate will be 20%.

For investment projects of enterprises specified at Point dd, Clause 1, Article 15 of this Decree which fail to satisfy the conditions specified at such Point within 3 years after being granted investment licenses (excluding the case of behind-schedule implementation due to delayed ground clearance or completion of administrative procedures by state enterprises or natural disasters or fires as approved by investment-licensing agencies and the Prime Minister) or after three years of turnover generation, these enterprises will not be entitled to the enterprise income tax incentives and shall declare and pay enterprise income tax amounts already declared for incentives in the previous years (if any) in accordance with law, but their previous tax declaration will not be regarded as false declaration under the law on tax administration. In a tax year within the duration of enjoyment of the enterprise income tax incentives, if an enterprise fails to fully satisfy one of the conditions for enjoyment of the tax incentives specified at Point dd, Clause 1, Article 15 of this Decree, it is not entitled to the enterprise income tax incentives in such year.

5. New investment projects eligible for the tax incentives specified in Clauses 1 and 3, Article 15 and Clauses 1, 2 and 3, Article 16 of this Decree are investment projects implemented for the first time or investment projects independent from ongoing projects, excluding:

a/ Investment projects formulated as a result of the separation, split, merger, consolidation or transformation of enterprises in accordance with law;

b/ Investment projects formulated as a result of the owner change (including cases of implementation of new investment projects with assets, business locations and business lines of former enterprises for continued production or business activities).

New investment projects eligible for the tax incentives specified in Articles 15 and 16 of this Decree must have investment licenses or investment certificates granted by competent state agencies. For a domestic investment project capitalized at under VND 15 billion and not on the list of conditional investment fields but associated with the establishment of a new enterprise, the document for identification of such investment project is the enterprise registration certificate.

Chapter V. IMPLEMENTATION PROVISIONS

Article 20. Effect

1. This Decree takes effect on February 15, 2014, and applies to the tax period from 2014 on.

To annul the Government’s Decrees No. 124/2008/ND-CP of December 11, 2008, and No. 122/2011/ND-CP of December 27, 2011, detailing and guiding a number of articles of the Law on Enterprise Income Tax, and Articles 2 and 3, the Government’s Decree No. 92/2013/ND-CP of August 13, 2013, detailing a number of articles of the Law Amending and Supplementing a Number of Articles of the Law on Enterprise Income Tax and the Law Amending and Supplementing a Number of Articles of the Law on Value-Added Tax which took effect on July 1, 2013.

2. Enterprises having investment projects which, by the end of the tax period of 2013, remain eligible for the enterprise income tax incentives, including also investment projects for which investment licenses, investment certificates or enterprise registration certificates have been granted (for domestic investment projects associated with the establishment of new enterprises, capitalized at under VND 15 billion and not on the list of conditional investment fields), and have not yet enjoyed the incentives under the legal documents on enterprise income tax before the effective date of this Decree may continue to enjoy the incentives for the remaining duration under such documents; in case they satisfy the conditions for enjoyment of the tax incentives specified in this Decree, they may choose to enjoy the incentives which they are currently entitled to or the incentives specified in this Decree (including tax rate incentives and tax exemption or reduction) for new investment for the remaining duration as enterprises newly established under investment projects or as expanded investment projects for the remaining duration.

Enterprises having investment projects eligible for the preferential tax rate of 20% specified in Clause 3, Article 15 of this Decree by the end of the tax period of 2015 may shift to apply the tax rate of 17% for the remaining duration from January 1, 2016.